Structural demand meets structural friction

Remittance inflows to Latin America and the Caribbean reached approximately $145 billion in 2023 - between 2% and 26% of GDP across recipient economies — and have grown at a compound annual rate of approximately 8% since 2010 despite cyclical volatility in source-country labour markets (World Bank, 2024). The persistence of this growth under varied macroeconomic conditions is inconsistent with a demand-constrained interpretation; it is more consistent with structural suppression by cost and accessibility barriers. At an average transfer cost of 5.7% on a $200 remittance — nearly double the G20's 3% target — a measurable share of potential volume remains priced out of formal channels.

The domestic modernisation experience provides a direct counterfactual. Brazil's Pix reached 140 million users within eighteen months of its November 2020 launch and processed over 42 billion transactions in 2023, displacing cash and card instruments at a pace that exceeded regulatory projections. The adoption curve confirms that payment demand is highly elastic with respect to friction reduction when infrastructure is made universally accessible.

The extension of Pix to cross-border use cases — live interoperability with Argentina's COELSA network, and bilateral frameworks with Uruguay, Chile, and Portugal — provides empirical evidence of latent regional demand that existing correspondent and public clearing infrastructure has not mobilised. Mexico's cash share of approximately 35% of point-of-sale volume and Central America's comparable figures are more plausibly explained by infrastructure gaps than by behavioural preference, a distinction with direct implications for policy design.

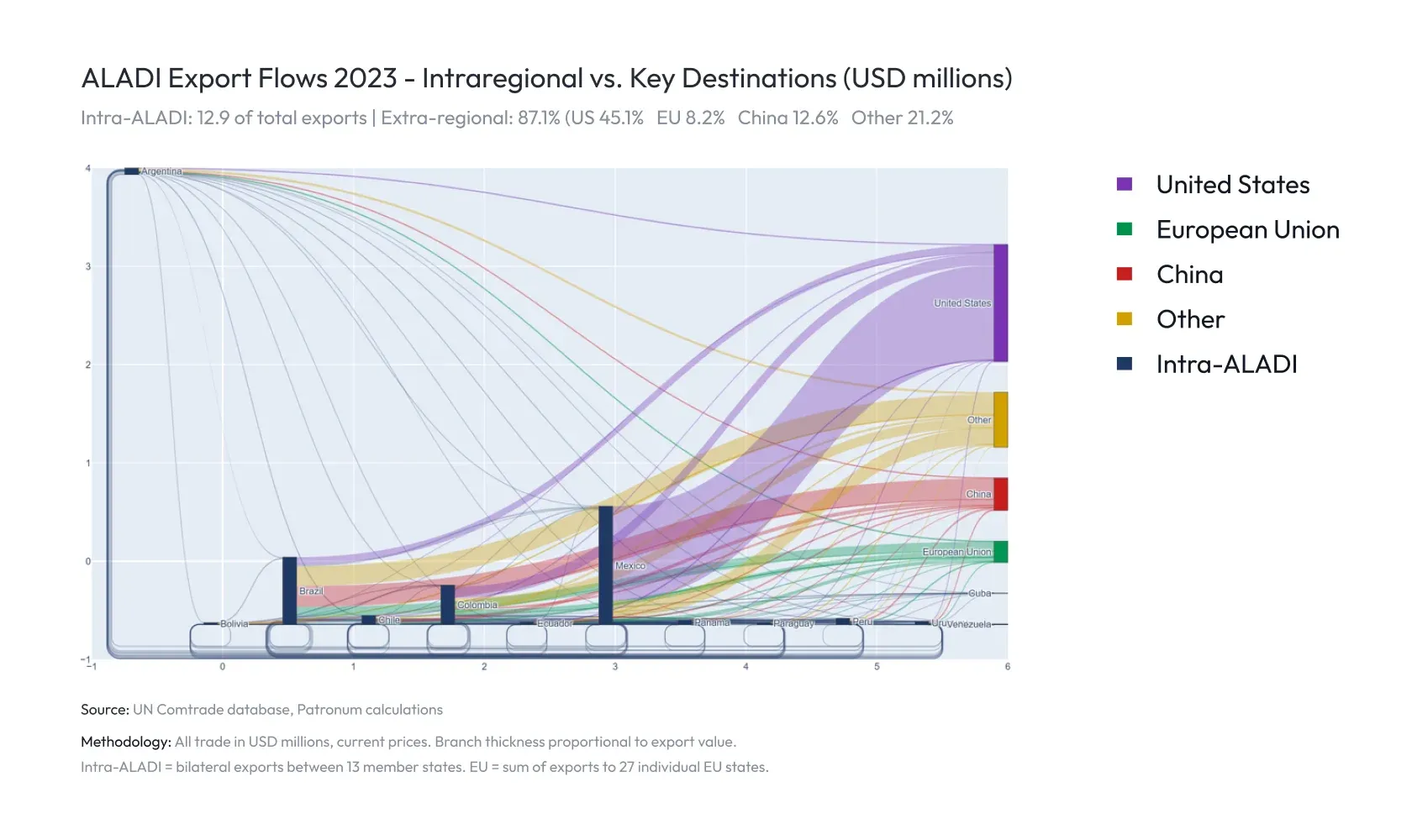

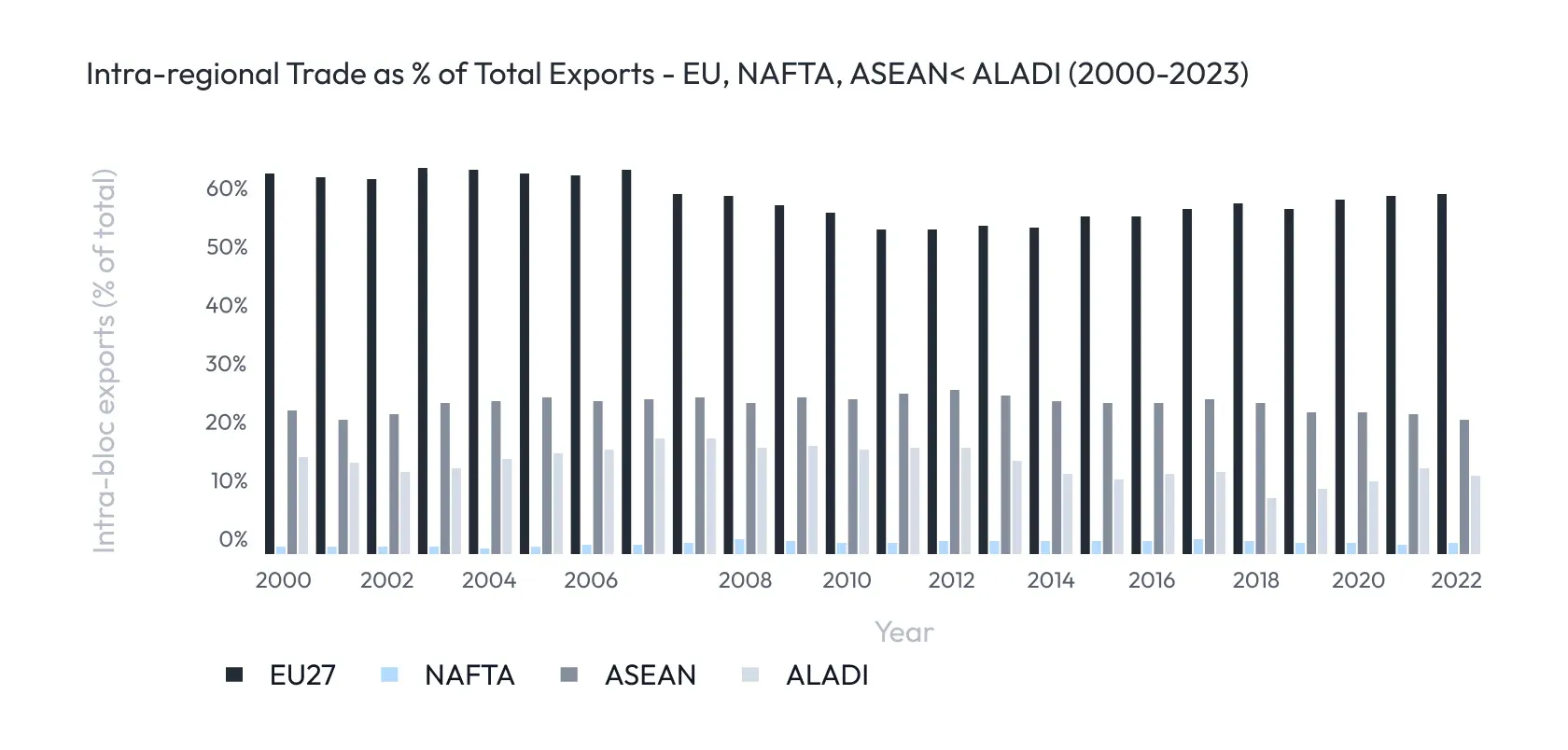

The trade dimension reinforces this diagnosis. Intraregional exports account for approximately 14% of total ALADI member exports — structurally stable over two decades, and well below ASEAN (25%), NAFTA/USMCA (40%), and the EU (60%). IMF gravity model estimates suggest Latin America's intraregional trade is 40–50% below the level predicted by economic fundamentals alone, with payment frictions identified as a specific additional explanatory variable (IMF, 2023).

Drakopoulos et al. (2024) estimate that a one percentage point reduction in cross-border payment fees is associated with a 15.2 percentage point increase in bilateral trade flows — significant at the 1% level — implying a trade-suppression effect from current intermediation costs that operates independently of tariff and non-tariff barriers. The mechanism runs through both transaction costs, which raise the effective price of cross-border commerce for SMEs lacking hedging capacity, and pre-funding requirements, which tie up working capital in nostro accounts and raise trade finance costs for smaller institutions in lower-volume corridors. Both effects are disproportionately concentrated in intra-LatAm corridors where correspondent relationships are thinnest and FX markets least liquid.

Why existing systems persist — and why alternatives fall short

The persistence of correspondent banking relationships reflects rational institutional equilibrium rather than inertia. CBRs provide settlement finality, compliance depth, and credit intermediation capacity that alternative architectures have not replicated at scale — advantages that are particularly material in a region characterised by heterogeneous regulatory frameworks and episodic macroeconomic instability. The FSB's de-risking surveys document a decline of approximately 20% in active CBR corridors serving Latin America and the Caribbean between 2011 and 2022. This contraction is better interpreted as a supply-side efficiency failure than as obsolescence: the corridors being abandoned are disproportionately those serving smaller economies and lower-volume flows, precisely where the fixed costs of bilateral trust-building are hardest to amortise.

Regional public alternatives have repeatedly encountered the same structural constraint. The Central American Clearing House, the CMCF, the ALADI CCR, and more recently SIPA have each demonstrated that centralised sovereign clearing in asymmetric currency unions is vulnerable to a predictable failure mode: deferred net settlement combined with bilateral credit extension among fiscally heterogeneous members produces imbalance accumulation that eventually exceeds the political capacity for burden-sharing. This pattern is consistent with the theoretical prediction of Adrian et al. (2023) that a clearinghouse reducing trust-link costs offers only marginal improvement over correspondent banking when it preserves the underlying architecture of sovereign credit exposure. SIPA's $2 billion in cumulative volume over fourteen years — against annual intraregional ALADI imports exceeding $180 billion — illustrates the scale ceiling that public wholesale infrastructure encounters when its cost and operating parameters exclude retail and SME flows.

Distributed ledger and stablecoin-based architectures address the settlement layer efficiently — atomic payment-versus-payment eliminates deferred clearing vulnerability — but introduce distinct constraints at the liquidity and governance layers. Without credible cross-jurisdictional liquidity pooling, thin decentralised pools produce slippage that is economically equivalent to the FX spread embedded in correspondent intermediation, as formalised by Adrian et al. (2023). The absence of a lender-of-last-resort function and unresolved questions of regulatory jurisdiction across permissionless networks further constrain institutional adoption. The technological frontier has produced instruments that are necessary but not sufficient for CBR substitution — a conclusion that points toward complementary rather than substitutive architectures as the near-term policy direction.

A transitional model: interoperability through orchestration

The G20 Cross-Border Payments Roadmap, updated in 2023, does not prescribe architectural uniformity. It prescribes interoperability as the organising principle — a distinction that is material for a region as heterogeneous as Latin America. The relevant policy question is accordingly not how to replace correspondent banking but how to reduce the marginal cost of connecting domestic payment infrastructures to cross-border flows without requiring convergence of underlying systems.

API-based orchestration platforms represent the most tractable near-term implementation. By standardising messaging — ISO 20022 providing the current international benchmark — compliance logic, and routing decisions at the platform layer, such architectures reduce the bilateral integration burden from an O(n²) problem, where each corridor requires a separate bilateral agreement, to an O(n) problem, where each participant connects once and accesses all connected corridors. The BIS CPMI (2022b) identifies this hub-and-spoke configuration as offering the most favourable scalability properties for regions with large numbers of heterogeneous domestic systems. Such platforms can remain structurally off-rail — facilitating coordination without directly participating in settlement — thereby preserving regulatory clarity and avoiding the lender-of-last-resort ambiguity that constrains DLT-based alternatives.

The practical architecture is hybrid. A retail cross-border transaction may be initiated through Pix or SPEI, routed through an orchestration layer handling FX rate discovery, compliance segmentation, and counterparty matching, and settled through existing correspondent channels where institutional relationships and settlement certainty justify the cost. Each component contributes its comparative advantage: the speed and near-zero marginal cost of domestic instant payment rails at the last-mile layer; the global reach and compliance depth of correspondent banking at wholesale settlement. Efficiency gains are concentrated precisely where current costs are highest — opaque fee chains, sequential bilateral FX conversion, and manual compliance processing.

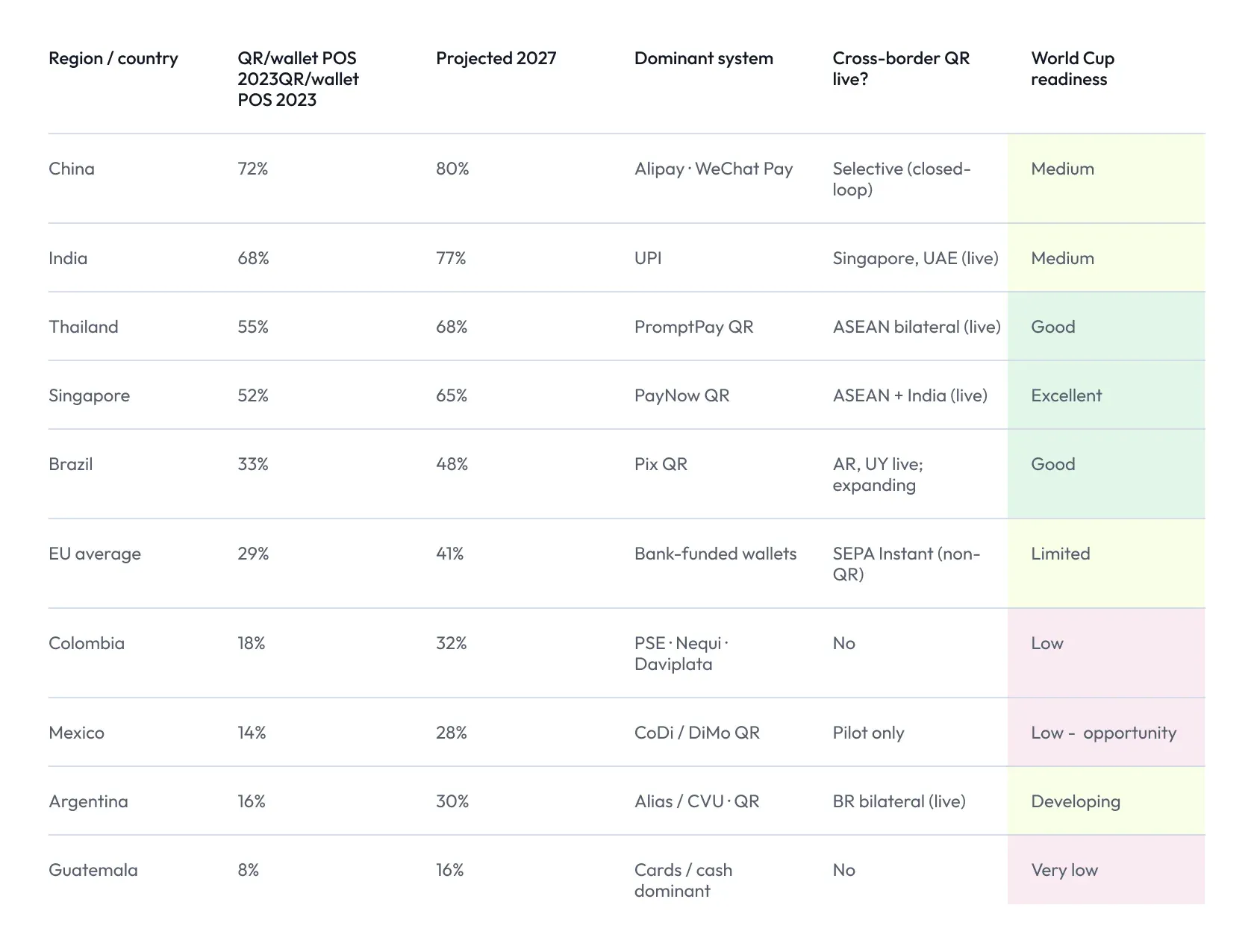

Cross-regional evidence supports the commercial viability of this model. The bilateral QR linkages between Singapore's PayNow, Thailand's PromptPay, and Malaysia's DuitNow have demonstrated rapid adoption without requiring users to alter domestic payment behaviour. The analogous infrastructure in Latin America — Mexico's CoDi/DiMo, Brazil's Pix QR, and the live Pix–COELSA corridor with Argentina — defines a nascent but technically functional cross-border QR network. The 2026 FIFA World Cup, projected to bring 5.5 million visitors to Mexican host cities including large contingents from Brazil, Argentina, and QR-native Asian markets, represents a time-bounded and commercially concrete demand event that could validate cross-border QR acceptance at scale, provided the orchestration layer connecting foreign wallets to domestic rails is operational ahead of the tournament.

Latin America's cross-border payments landscape presents strong and growing demand, fragmented and partially contracting supply-side infrastructure, and an emerging set of complementary technologies that are individually insufficient but jointly promising. Correspondent banking retains genuine comparative advantage in the high-value, compliance-intensive segment. Domestic fast payment modernisation has confirmed that latent demand responds sharply to friction reduction. International policy consensus has converged on interoperability as the achievable and stability-preserving objective. The most robust near-term path connects all three: API-native orchestration platforms that augment correspondent channels with domestic fast payment connectivity, standardised through ISO 20022, governed through bilateral PSP agreements rather than sovereign credit arrangements, and validated through large-scale international tourism before scaling across the full breadth of intraregional trade and remittance flows.

1. The Paradox of Modern LatAm Payments

Latin America presents one of the most striking paradoxes in global finance. The region is home to two of the world's most sophisticated domestic payment infrastructures - Brazil's Pix and Mexico's SPEI - yet cross-border payments between its own economies remain among the most fragmented, expensive, and poorly served in the world.

Pix processed over 224 million transactions in a single day in early 2025, surpassing the combined Brazilian volume of major international card networks. SPEI settles billions in domestic transfers daily at near-zero marginal cost. And yet a Brazilian merchant wishing to pay a Colombian supplier, or a Guatemalan family sending money to relatives in Mexico, must navigate a correspondent banking system that has served the global economy for decades - but which charges flat fees, operates on banking hours, and routes through major financial centres regardless of the actual geography of the transaction.

It is important to note at the outset that correspondent banking relationships (CBRs) remain the backbone of international payments globally. They have built the trust infrastructure, compliance frameworks, and settlement certainty that underpin trillions of dollars in annual flows. The argument advanced in this paper is not that CBRs should be displaced - they serve a critical function, particularly for high-value, time-insensitive, and complex cross-border transactions. Rather, the argument is that CBRs alone cannot efficiently serve the full spectrum of cross-border payment demand in Latin America, particularly at the retail, remittance, and SME end of the market, and that API-native interlinking of domestic fast payment systems (FPS) can complement and extend the correspondent banking model where it is structurally constrained.

The root structural constraint is not technology. It is architecture: the CBR model was designed for a world where trust had to be established bilaterally, currency risk warehoused in nostro accounts, and settlement deferred across multiple business days. As the IMF has documented, this model - while functioning well for major currency corridors - is not only expensive at the margins but actively contracting for smaller LatAm economies, as global banks retreat from lower-volume emerging market corridors due to the fixed costs of maintaining bilateral trust relationships.

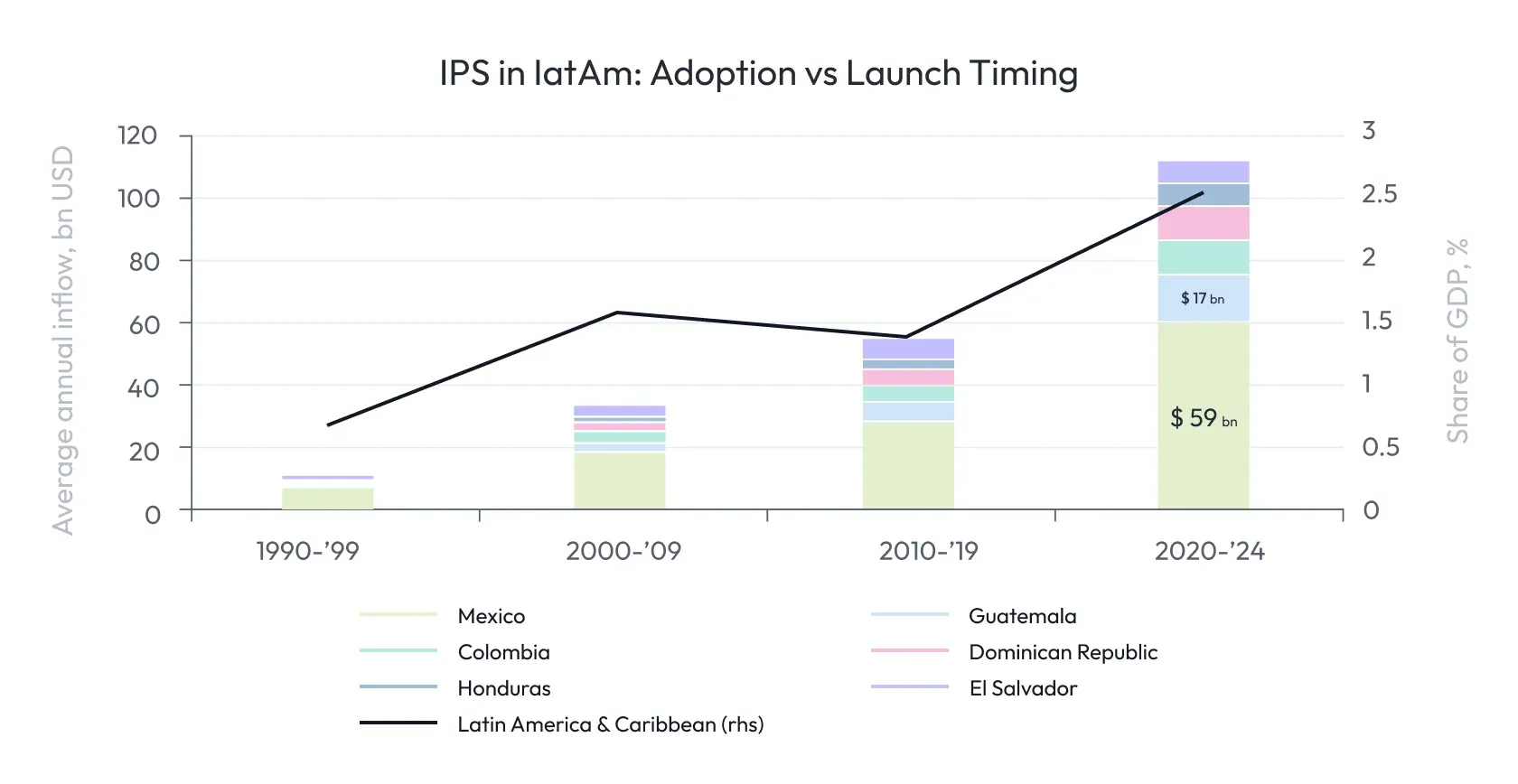

The remittance data illustrates the scale of the demand that the current architecture underserves. Latin America's top six recipient economies collectively receive over $120 billion annually in remittances - a figure that has grown threefold since 2000. These flows represent the most price-sensitive, last-mile cross-border payment use case, and the one most constrained by the fixed-fee, banking-hours architecture of the correspondent model.

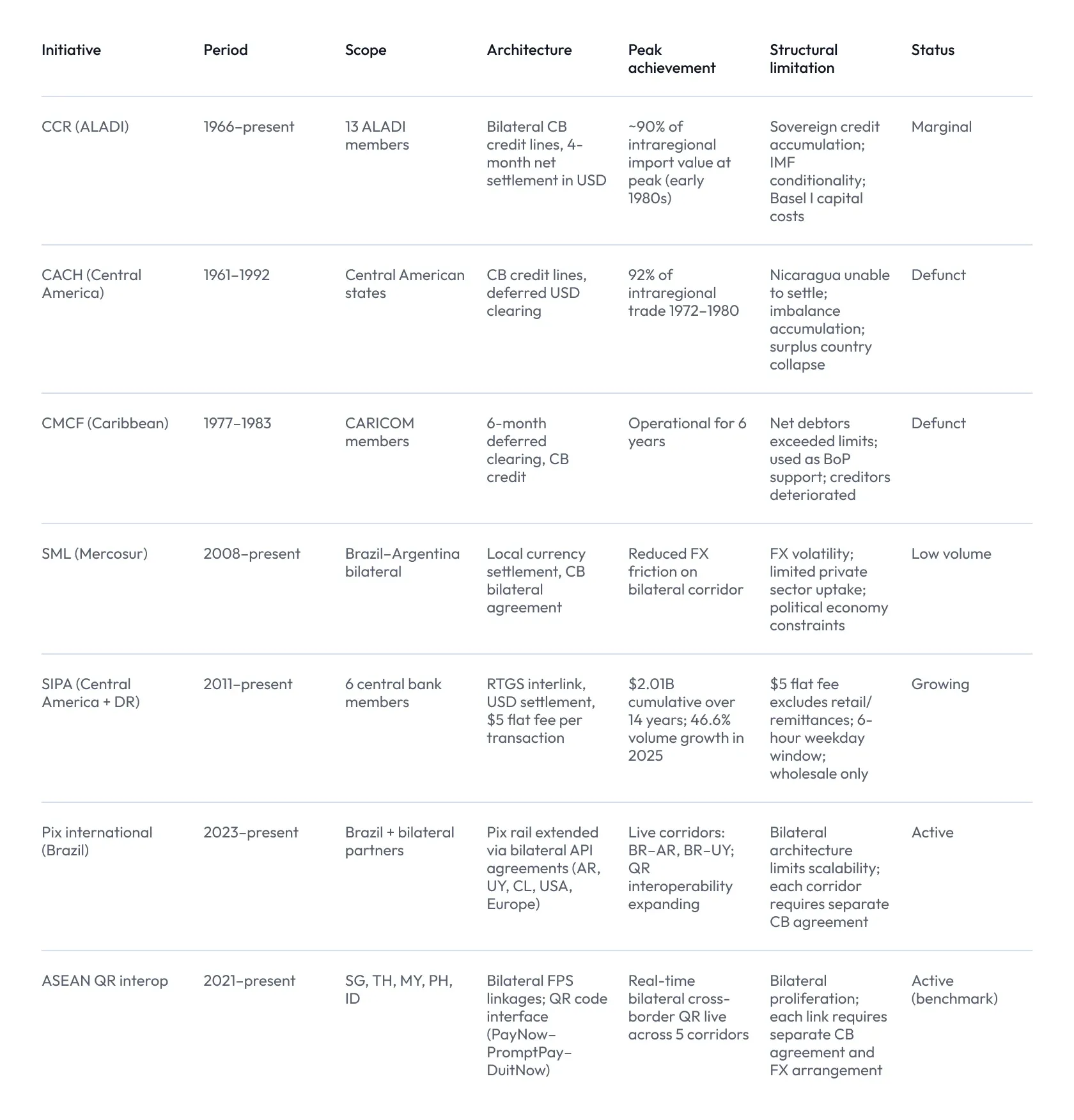

2. A History of Regional Integration Attempts

The history of LatAm payment integration is not a story of insufficient ambition. It is a story of correct diagnosis and structurally constrained architecture, repeated across six decades. Each initiative correctly identified that payment friction was suppressing regional trade. Each designed a solution that ultimately encountered the same fundamental barrier: the need to pool credit risk among sovereign institutions with asymmetric fiscal positions and volatile exchange rates.

The following table summarises the major regional payment initiatives and their structural characteristics.

2.1 The Central American and Caribbean experience

The Central American Clearing House (CACH) represents the most instructive case study. At its peak between 1972 and 1980, CACH channelled 92% of intraregional trade - a remarkable achievement that demonstrates the potential of regional payment integration when political and institutional conditions are favourable. Its collapse in the early 1980s, triggered by Nicaragua's incapacity to settle its accumulated obligations, illustrates the structural vulnerability that any credit-based sovereign clearing arrangement inherits: the system is only as strong as its weakest member's fiscal position.

The Caribbean Community Multilateral Clearing Facility (CMCF) repeated the same failure mode within six years. The six-month settlement window - designed to provide operational flexibility - instead allowed imbalances to compound beyond the capacity of creditor members to absorb. The facility collapsed when it was effectively being used as a balance-of-payments support mechanism rather than a payment infrastructure.

Both cases confirm the theoretical prediction advanced by Adrian et al. (IMF Fintech Note 2023/001): a global or regional clearinghouse that reduces the cost of establishing trust links offers only marginal improvement to the correspondent banking arrangement when it preserves the fundamental architecture of bilateral sovereign credit exposure. The problem is not the design of the clearinghouse - it is the architecture of deferred, credit-based settlement among asymmetric sovereigns.

2.2 SIPA: progress and structural ceiling

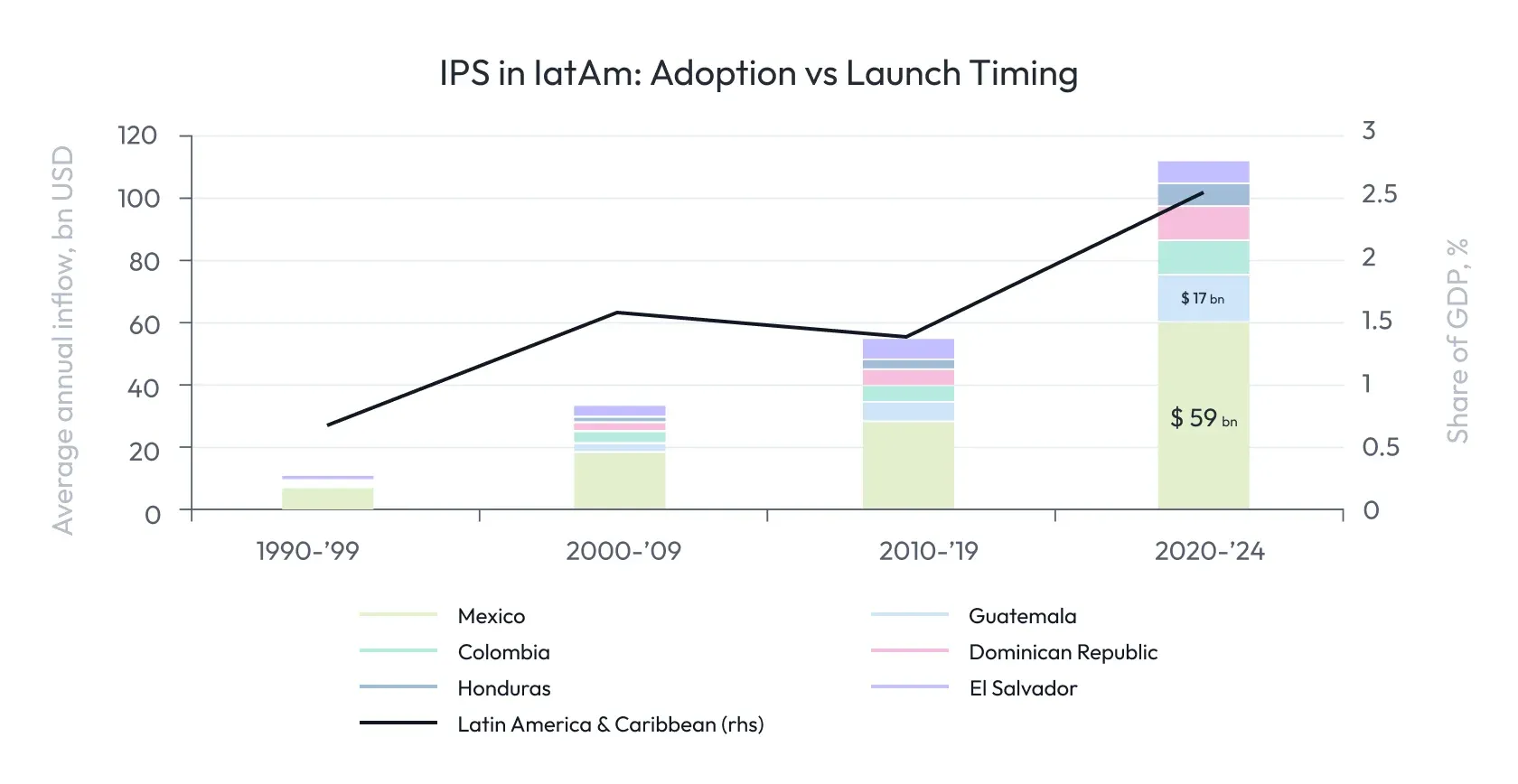

The Sistema de Interconexión de Pagos (SIPA), operated by the central banks of Central America and the Dominican Republic since 2011, represents the most technically mature current public cross-border payment system in the region. Its 46.6% volume growth in 2025 and interconnection of 77 financial institutions demonstrate that real-time interbank settlement across borders is operationally achievable.

However, SIPA's structural parameters reveal its ceiling. The $5 flat fee per transaction makes the system economically viable only for relatively large transfers - at $50 transaction value the fee represents a 10% cost, well above the G20's 3% target for remittances. The 6-hour weekday operating window is incompatible with retail commerce. And SIPA's $2.01 billion cumulative volume over fourteen years amounts to less than two weeks of total ALADI intraregional imports - illustrating the scale mismatch between the public payment infrastructure and the actual trade flows it was designed to serve.

3. The Scale of the Opportunity

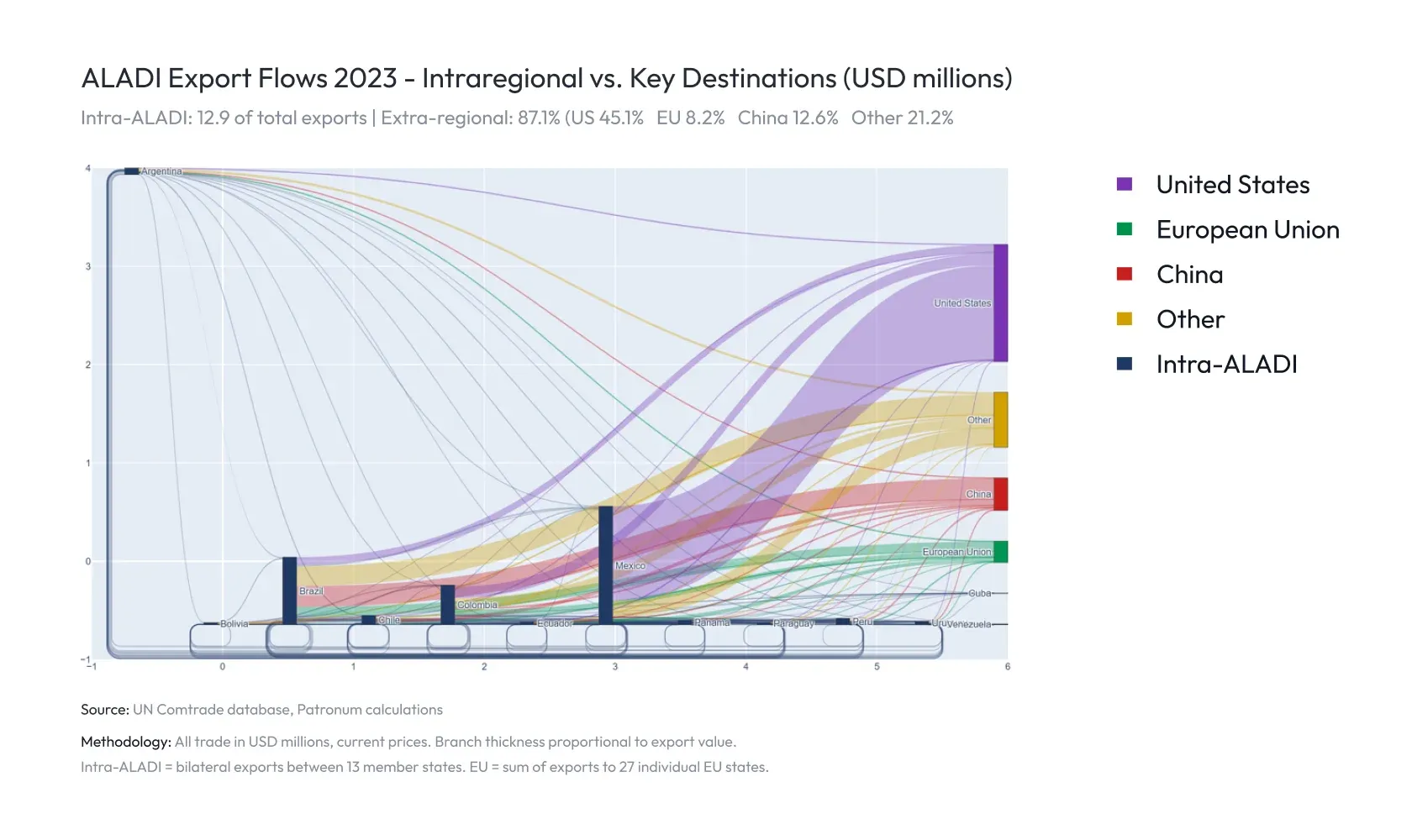

The intraregional trade data exposes the opportunity in its starkest form. ALADI's intraregional trade accounts for approximately 14% of its members' total exports - a figure comparable to Sub-Saharan Africa and less than half of ASEAN's approximately 25% share. The EU's 60% and NAFTA's 40%+ intraregional shares represent the upper benchmark of what deep trade and payment integration can sustain over time.

The IMF's own gravity model estimates that a reduction of one percentage point in cross-border transaction fees would lead to a 15.2 percentage point increase in bilateral trade flows - a statistically significant finding at the 1% level. This estimate implies that the structural payment friction embedded in the current correspondent model is a material drag on LatAm's intraregional trade performance, beyond the infrastructure, governance, and commodity structure factors typically cited in the literature.

The World Cup in 2026, hosted across Mexico City, Guadalajara, and Monterrey, creates a specific and time-bounded context in which this payment friction becomes directly observable. Fans from 212 countries have purchased tickets, with the largest contingents from England, Germany, Brazil, Colombia, Spain, Argentina, and France - a mix of European bank-transfer users, Brazilian Pix users, and card-dominant markets. Each of these visitors will encounter Mexico's payment infrastructure, which today cannot efficiently process payments from foreign wallets or fast payment systems without going through traditional card network or correspondent banking channels.

4. Structural Limitations of the Proposed Alternatives

The international policy community has proposed two principal responses to the constraints of correspondent banking. Both merit careful analysis, as each addresses part of the problem while carrying structural limitations of its own - particularly in the LatAm context.

4.1 Global CCP and swap line extension

The first proposal is a global central counterparty (CCP) clearinghouse that intermediates swap arrangements between central banks - essentially a multilateral version of the CACH architecture, modernised with rigorous collateral requirements. Adrian et al. (2023) identify two structural limitations. First, political backing for risk-sharing arrangements among sovereigns is structurally difficult to sustain: even the IMF, the most institutionally robust multilateral risk-sharing arrangement ever constructed, operates under strict governance and conditionality precisely to manage the fiscal instability that unconstrained sovereign credit pooling produces. Second, at the technical level, collateral requirements for less liquid currency pairs become prohibitive. The FX spreads and margin call dynamics for intra-LatAm crosses - MXN/BRL, COP/PEN - are substantially less favourable than for major reserve currency pairs, creating a structural tendency toward exclusion of smaller economies.

Importantly, these are limitations of the centralised CCP model as a standalone solution - not arguments against the correspondent banking system itself, which remains essential for the high-value, complex transactions where its trust and compliance infrastructure is difficult to replicate.

4.2 Trust networks for tokenised money

The second proposal focuses on building trust networks for tokenised forms of central bank and commercial bank money. Adrian and Mancini-Griffoli (2023) note that the costs of establishing trust links with multiple private money issuers can, at first, exceed those of the traditional banking system, as competition among issuers multiplies the sunk costs users must bear. A fragmented landscape of CBDCs, stablecoins, and tokenised deposits - each requiring separate trust infrastructure - risks reproducing the correspondent banking concentration problem at the digital layer rather than resolving it.

Bitcoin illustrates the outer limit of decentralised settlement. The Bitcoin network has operated uninterrupted for over a decade, demonstrating that protocol-level trust without institutional intermediaries is technically achievable. However, the energy intensity of proof-of-work consensus, the anonymity of transactions (which precludes AML/CFT compliance), and the volatility of the asset make it unsuitable as a settlement instrument for commercial payment flows. A better solution is needed - one that preserves the trust and finality advantages of decentralised settlement while meeting the policy requirements of regulated payment systems.

5. LatAm's Structural Enablers

The critique of pre-funded correspondent banking - that it concentrates liquidity in major currencies, warehousing exotic pairs at prohibitive cost - carries less force in a region that has already partially solved the anchor currency problem through dollarization and USD-denominated trade invoicing.

Ecuador, El Salvador, and Panama are fully dollarized. Bolivia, Peru, Paraguay, and Uruguay maintain foreign currency deposit ratios of 45–75% of total bank deposits. The dominant invoicing currency for intra-LatAm commodity trade is USD even between non-dollarized countries, and the US–Mexico remittance corridor - the world's largest single bilateral remittance flow at over $63 billion annually - is overwhelmingly USD-denominated.

In practical terms, an API-native FX settlement layer in LatAm does not need to warehouse exotic bilateral currency pairs. It needs to efficiently route USD-equivalent value to local last-mile rails where conversion to MXN or BRL occurs at the deepest available FX market - the USD/local currency spot market - rather than at a thin bilateral exotic cross. This is structurally simpler than the global XC platform concept envisions for regions without a dominant settlement currency anchor.

Stablecoin adoption reinforces this structural advantage. Argentina, Venezuela, Brazil, and Mexico consistently rank among the top 20 globally for stablecoin transaction volumes, driven by dollar demand in high-inflation economies and friction in accessing formal USD banking. USD-pegged stablecoins such as USDC provide a liquid, low-cost bridge for the API settlement layer that eliminates currency warehousing without requiring wholesale CBDCs to be production-ready. Brazil's Drex project, Mexico's digital peso initiative, and Colombia's CBDC pilot are all in active development - and when they reach production readiness, the API architecture accommodates them without redesign, providing a long-term upgrade path that preserves continuity with existing correspondent relationships.

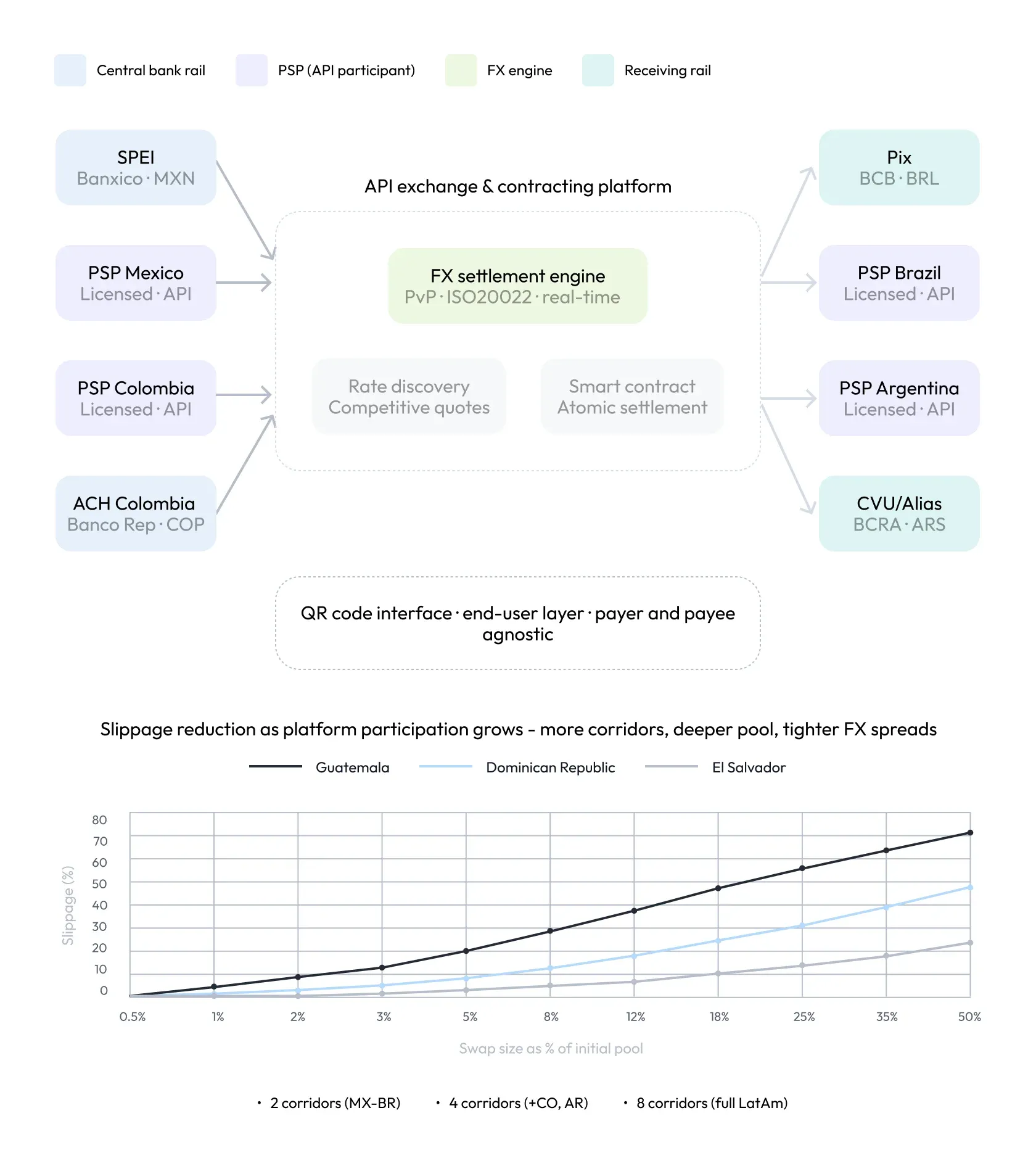

6. The API Exchange and Contracting Platform

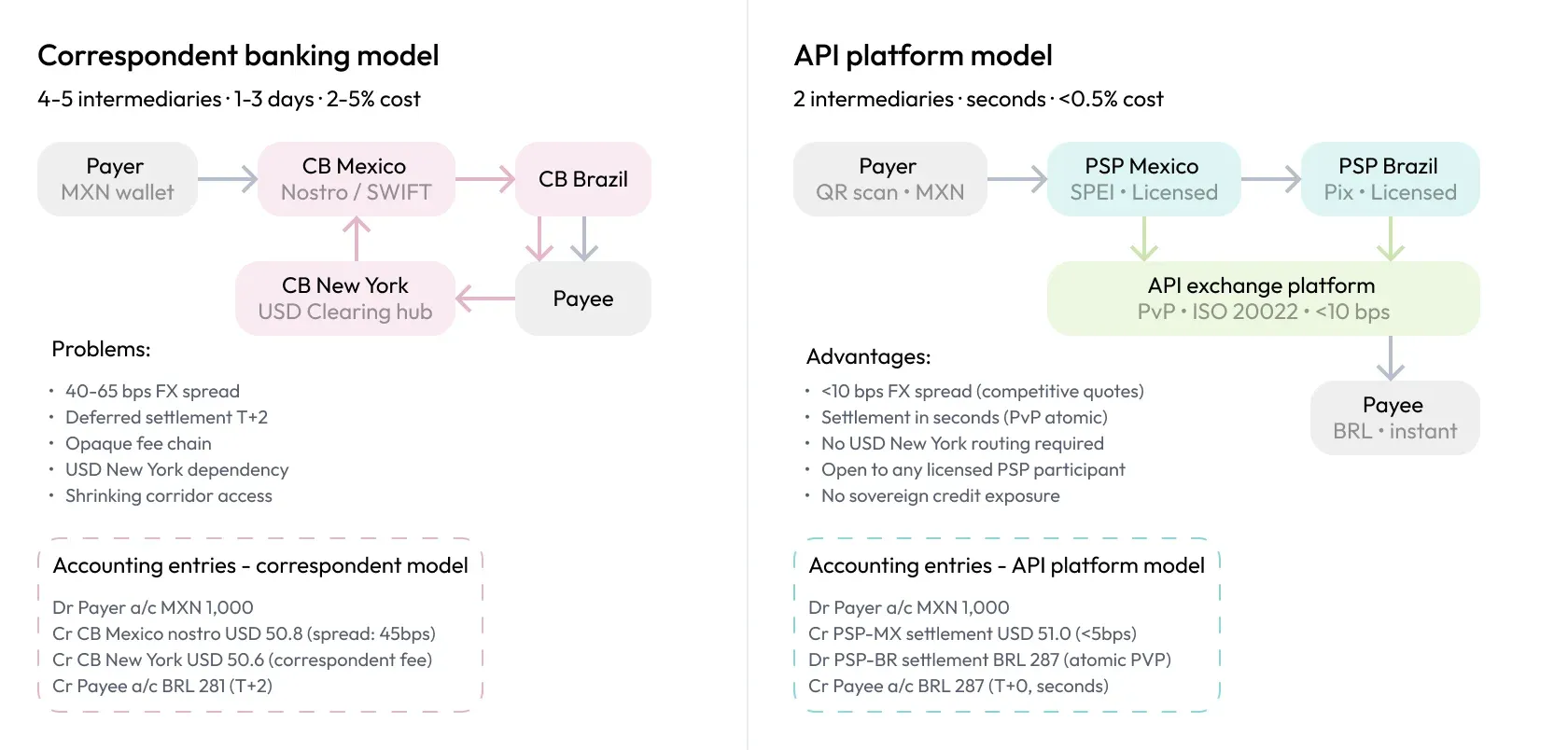

The architecture proposed draws directly from the XC platform framework developed by Adrian and Mancini-Griffoli (IMF Fintech Note 2023/005), adapted to LatAm's dollarization context and existing fast payment infrastructure. The key architectural departure from both the correspondent banking model and the tokenised marketplace concept is that FX conversion occurs through competitive real-time quotes from licensed PSP participants rather than through pre-funded nostro accounts or automated market maker pools.

This distinction has significant implications for capital efficiency. Under the correspondent model, a bank must maintain pre-funded balances in each currency it settles - the nostro account - creating idle capital that earns below-market returns. Under the API model, FX conversion is arranged at the moment of settlement through competitive market quotes, with no party required to warehouse currency inventory. The IMF's own analysis of correspondent banking notes that the industry is concentrated precisely because the fixed costs of building trust and managing warehousing risks create barriers to entry. An API-native model with competitive quote discovery lowers these barriers structurally.

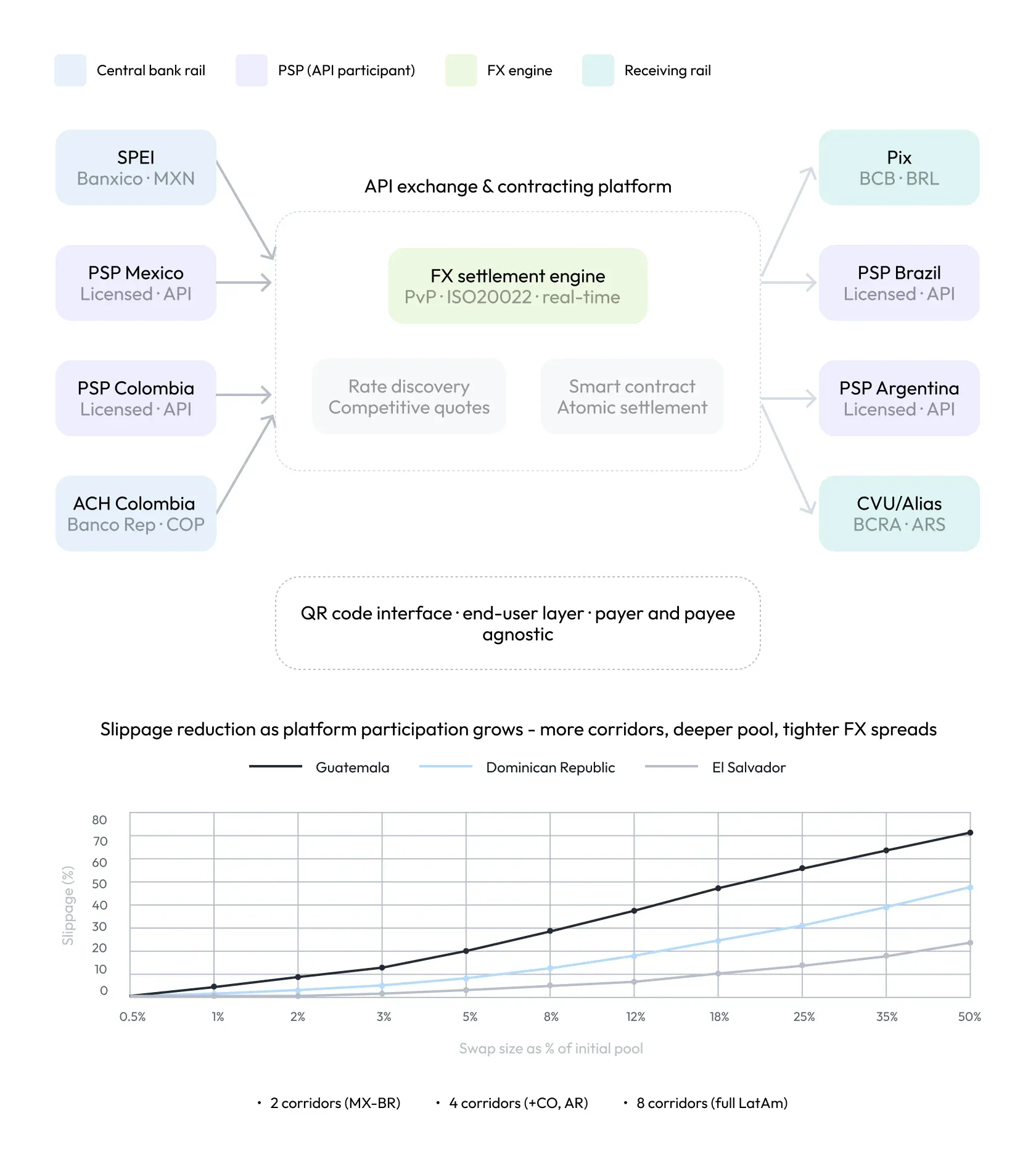

The interlinking framework described by the BIS (CPMI, 2022b) identifies four models for connecting payment systems across borders: single access point, bilateral link, hub-and-spoke, and common platform. The API exchange and contracting platform described here is closest to the hub-and-spoke model - a single connection point for multiple domestic FPS operators, reducing the bilateral agreement proliferation that currently constrains Pix's international expansion to one corridor at a time.

6.1 Slippage and the network effect

A critical property of the competitive quote model is that pricing improves with participation. The slippage between the quoted rate and the realised settlement rate - analogous to the bid-ask spread in traditional FX - falls as more PSPs compete to fill each transaction. Adrian et al. (2023) formalise this relationship in the context of tokenised liquidity pools; the equivalent dynamic in the API quote model is that a broader participant base creates deeper effective liquidity without requiring any individual participant to warehouse more currency.

At two corridors (Mexico–Brazil), API-native spreads are estimated at 20–30 basis points - already competitive with correspondent banking for medium-value transactions. At four corridors adding Colombia and Argentina, this falls below 15 basis points. A full ALADI-scale platform approaches the 10 basis point threshold that makes the model competitive with international card networks for transactions above approximately $50.

6.2 The role of correspondent banks in the new architecture

It is important to be precise about the relationship between the proposed API layer and the existing correspondent banking infrastructure. The two are complementary rather than competing. Correspondent banks retain their comparative advantage in: high-value institutional flows where compliance depth and settlement certainty are paramount; complex multi-currency transactions requiring sophisticated hedging; markets where fast payment infrastructure is not yet mature; and jurisdictions with regulatory requirements that mandate bank intermediation.

The API layer addresses the segment where correspondent banking is structurally constrained: retail payments, remittances, SME cross-border commerce, and tourist transactions, all of which share a low average transaction value that makes the fixed costs of correspondent intermediation disproportionate. In this segment, the correspondent model's cost structure - flat fees, deferred settlement, opacity of fee chains - creates a price floor that excludes a substantial share of potential demand.

The proposed architecture effectively segments the market by transaction type rather than by geography or institutional relationship, allowing correspondent banks to focus on their highest-value flows while API-native infrastructure serves the retail and SME segment. This is consistent with the G20 Roadmap for Enhancing Cross-Border Payments' emphasis on payment system interoperability and complementary rather than competing infrastructure.

7. The QR Code as Universal Interface

The final architectural element is the user interface layer. The API exchange platform's FX engine and routing logic are invisible to the end user. What the user interacts with - whether they are a tourist scanning a restaurant code or an SME processing a supplier payment - is a QR code.

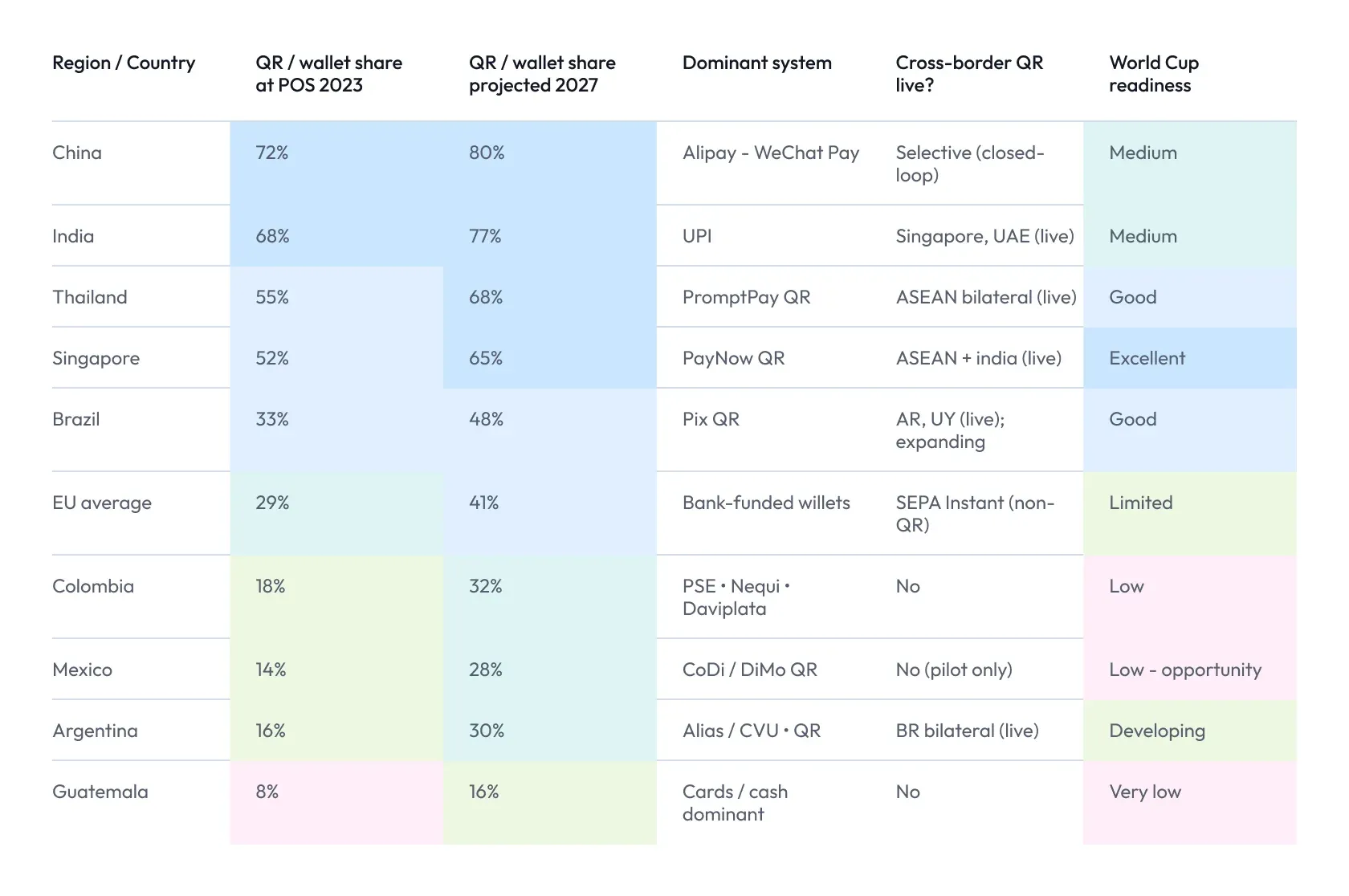

The QR code is architecturally significant because it is the one payment interface that is already implemented on both closed-loop and open-loop systems across all three regions relevant to this analysis. The BIS has noted that cross-border retail payments often rely on closed-loop systems - single platforms connecting both payee and payer - which creates fragmentation, as each platform requires bilateral enrollment. The QR standard breaks this fragmentation: a wallet app reads the same QR regardless of whether the underlying settlement happens on Pix, SPEI, a licensed PSP rail, or a card network.

The ASEAN experience provides the most relevant empirical benchmark. The bilateral linkages between PayNow (Singapore), PromptPay (Thailand), and DuitNow (Malaysia) demonstrate that QR-based cross-border payments can be live, real-time, and cost-effective without requiring a new centralised platform - the QR is the common interface, and the underlying settlement arrangement is bilateral and pragmatic. The Juniper Research forecast of 590% growth in Southeast Asian QR cross-border payments by 2028 reflects adoption of an already-proven model rather than a speculative projection.

8. Policy Implications and Governance

The architecture described requires three categories of policy enablement, none of which involves the sovereign credit pooling that has historically undermined LatAm payment integration.

First, bilateral API agreements between licensed PSPs across jurisdictions - analogous to the correspondent banking agreements that already exist, but operating at the PSP rather than the central bank level. These agreements govern technical standards (ISO 20022 messaging, API protocol specifications), compliance responsibilities (AML/CFT obligations, data localisation), and dispute resolution. The BIS interlinking framework provides a template for these agreements that does not require central bank treaty-level commitment.

Second, regulatory recognition of licensed PSPs as eligible participants in cross-border payment arrangements - currently a gap in several LatAm jurisdictions where only commercial banks are authorised to initiate cross-border transfers. Mexico's fintech law and Brazil's payment institution framework are the most advanced in the region; extending similar frameworks to Colombia, Peru, and Chile would complete the regulatory preconditions for multi-corridor API interlinking.

Third, and most importantly for the medium term, FX settlement arrangements that allow USD-stablecoin intermediation on the bridge leg without triggering VASP licensing requirements that vary significantly across the region. The IMF's assessment of CBDCs notes that wholesale digital currencies can eventually serve this function within the same architecture - making the stablecoin bridge a transitional arrangement rather than a permanent dependency.

Throughout all of this, the governance role of regional institutions - ALADI, the Central American Council of Monetary Board Presidents (CMCA), and CARICOM's financial regulators - is to harmonise the technical and compliance standards that enable bilateral PSP agreements to scale. This is a substantially lighter governance burden than the sovereign credit pooling that previous integration attempts required, and it builds on existing institutional relationships rather than requiring new treaty frameworks.

9. Conclusion

The narrative of Latin American payment integration is typically told as a story of political fragmentation - too many currencies, too much macroeconomic volatility, too little institutional trust between sovereigns. This analysis suggests a more precise diagnosis: every sustained integration attempt has tried to build sovereign credit infrastructure, and sovereign credit infrastructure in an asymmetric, FX-volatile region will encounter the same structural failure mode regardless of institutional design.

The combination of modern domestic fast payment rails, regional dollarization, stablecoin adoption at scale, and a maturing licensed PSP ecosystem creates, for the first time, the enabling conditions for a complementary architecture - one that does not require sovereign credit pooling, does not warehouse exotic currency pairs, and does not depend on banking-hours RTGS windows. This architecture does not displace the correspondent banking relationships that serve the region's high-value institutional flows; it extends the reach of the payment system into the retail, SME, and remittance segment where the correspondent model's cost structure creates a price floor that excludes substantial demand.

The global payment integration initiatives championed by the G20 roadmap, the BIS Innovation Hub's Project Nexus, and the IMF's XC platform framework all point in the same architectural direction: competitive, open, API-native interlinking of domestic fast payment systems through contractual and technical frameworks rather than sovereign credit arrangements. Latin America's specific structural characteristics - dollarization, stablecoin penetration, and the scale of Pix and SPEI - mean the region is unusually well-positioned to move toward this model ahead of other emerging market regions.

The 2026 World Cup in Mexico provides a concentrated test case: millions of visitors from QR-native payment markets - Brazil, ASEAN, China - arriving in a country with sophisticated but domestically-oriented QR infrastructure. Bridging that gap, for that event, with an API layer connecting CoDi/SPEI to Pix and foreign wallet networks, would demonstrate at scale what the literature has argued in theory: that payment architecture, not political will, has been the binding constraint on LatAm's cross-border integration.

References

Adrian, T. and Mancini-Griffoli, T. (2023). The Rise of Payment and Contracting Platforms. IMF Fintech Note 2023/005. International Monetary Fund, Washington, DC.

Adrian, T., Garratt, R., He, D. and Mancini-Griffoli, T. (2023). Trust Bridges and Money Flows: A Digital Marketplace to Improve Cross-Border Payments. IMF Fintech Note 2023/001. International Monetary Fund, Washington, DC.

Banco Central do Brasil (2025). Pix Statistics. Available at: bcb.gov.br/en/monetarycreditpolicy/pixstatistics.

BIS Committee on Payments and Market Infrastructures (2022a). Annual Economic Report 2022, Chapter III: The future monetary system. Bank for International Settlements, Basel.

BIS Committee on Payments and Market Infrastructures (2022b). Interlinking payment systems and the role of application programming interfaces. CPMI Papers No. 209. Bank for International Settlements, Basel.

Drakopoulos, D., Mu, Y., Vasilyev, D. and Villafuerte, M. (2024). Cross-Border Payments Integration in Latin America and the Caribbean. IMF Working Paper WP/24/119. International Monetary Fund, Washington, DC.

FSB Financial Stability Board (2020). Enhancing Cross-border Payments: Stage 3 Roadmap. Financial Stability Board, Basel.

G20 (2023). G20 Roadmap for Enhancing Cross-Border Payments: Prioritised Actions for Achieving the G20 Targets. Third Update.

Guerra-Borges, A. (1996). El comercio intrarregional centroamericano: tendencias y perspectivas. CEPAL, Mexico.

IMF (2023). Western Hemisphere Regional Economic Outlook. International Monetary Fund, Washington, DC.

Juniper Research (2024). Cross-Border Payments: Key Trends, Strategies & Market Forecasts 2024–2028.

Miller, R. (1993). The Caribbean Community Multilateral Clearing Facility: An Assessment. Economic Review, Eastern Caribbean Central Bank.

Ocampo, J.A. and Titelman, D. (2012). Regional Monetary Cooperation in Latin America. BIS Paper No. 63. Bank for International Settlements, Basel.

UN Comtrade (2025). International Trade Statistics. Available at: comtradeplus.un.org.

Worldpay (2025). Global Payments Report 2025. FIS / Worldpay.

World Bank (2025). Remittance Prices Worldwide. Available at: remittanceprices.worldbank.org.