Yet, beneath this shared success lies a sharp divergence in how these systems were built. Some central banks acted as builders and operators of public infrastructure, while others functioned strictly as regulators of private-sector innovation. These differing “institutional paths” have led to vastly different adoption results:

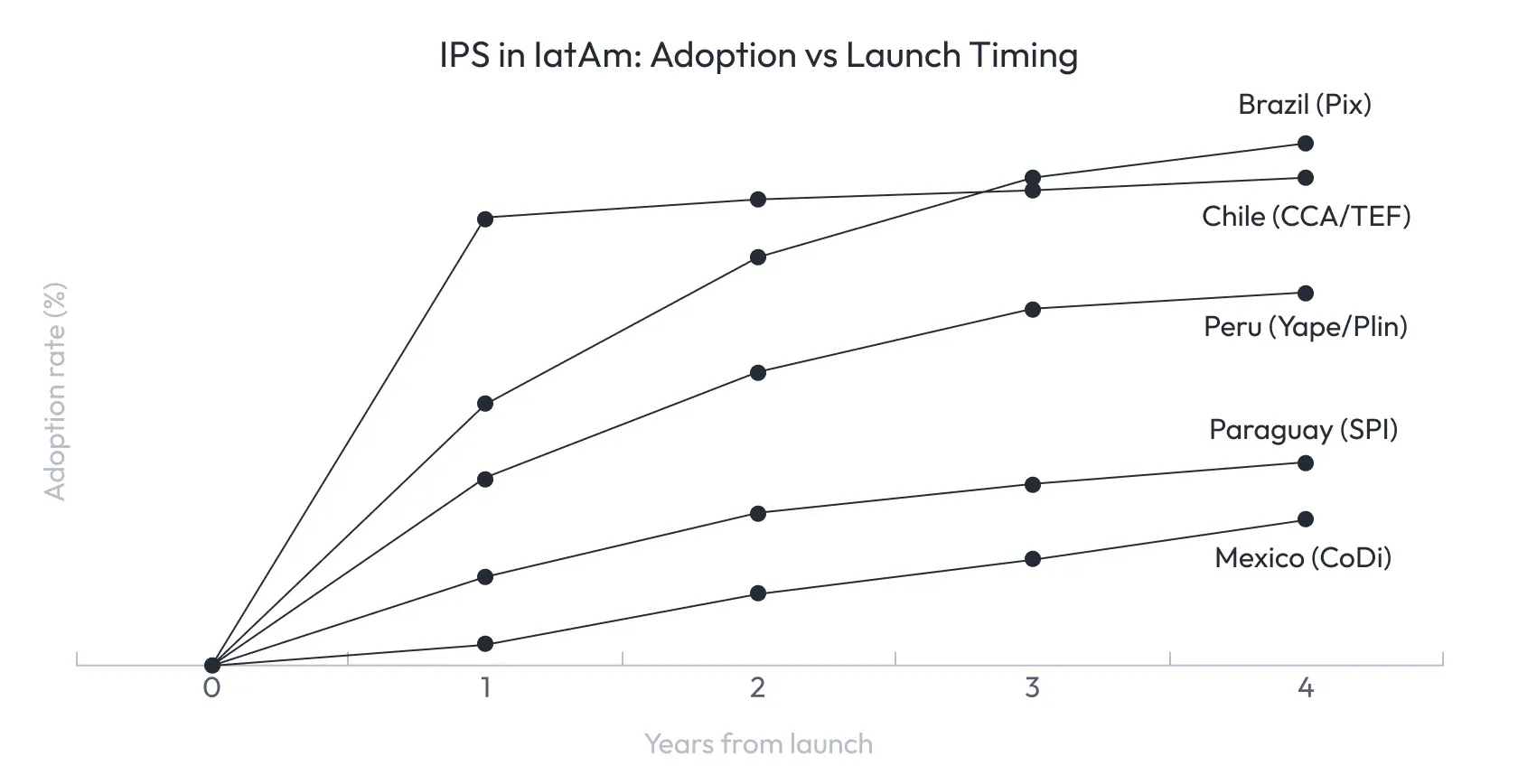

Mexico’s CoDi, a state-led utility launched in 2019, has struggled with adoption, with only about 20% of the adult population registered as of late 2024. Yet Mexico also hosts one of Latin America’s most dynamic fintech ecosystems — ranking as the region’s second-largest market with over 800 domestic fintech companies and more than 1,100 including foreign entrants, concentrated in payments, lending, and digital services — and attracting a significant share of regional venture capital.

Peru’s Yape and Plin, which began as private “walled gardens,” saw their reach explode to over 65% of adults after a 2022 central bank mandate forced them to become interoperable. However, the country still demonstrates a very high share of cash (45%) in circulation despite the fintech boom.

This contrast raises a fundamental question: which institutional model best supports financial inclusion while still fostering fintech innovation and competition?

How Latin America Built Instant Payments: Three Institutional Paths

While the technical ambition is similar across countries — speed, accessibility, and affordability — the business models governing IPS in Latin America differ sharply. These differences reflect distinct policy choices regarding the role of the central bank, the allocation of operational and liquidity risk, and the incentives provided to banks and fintechs.

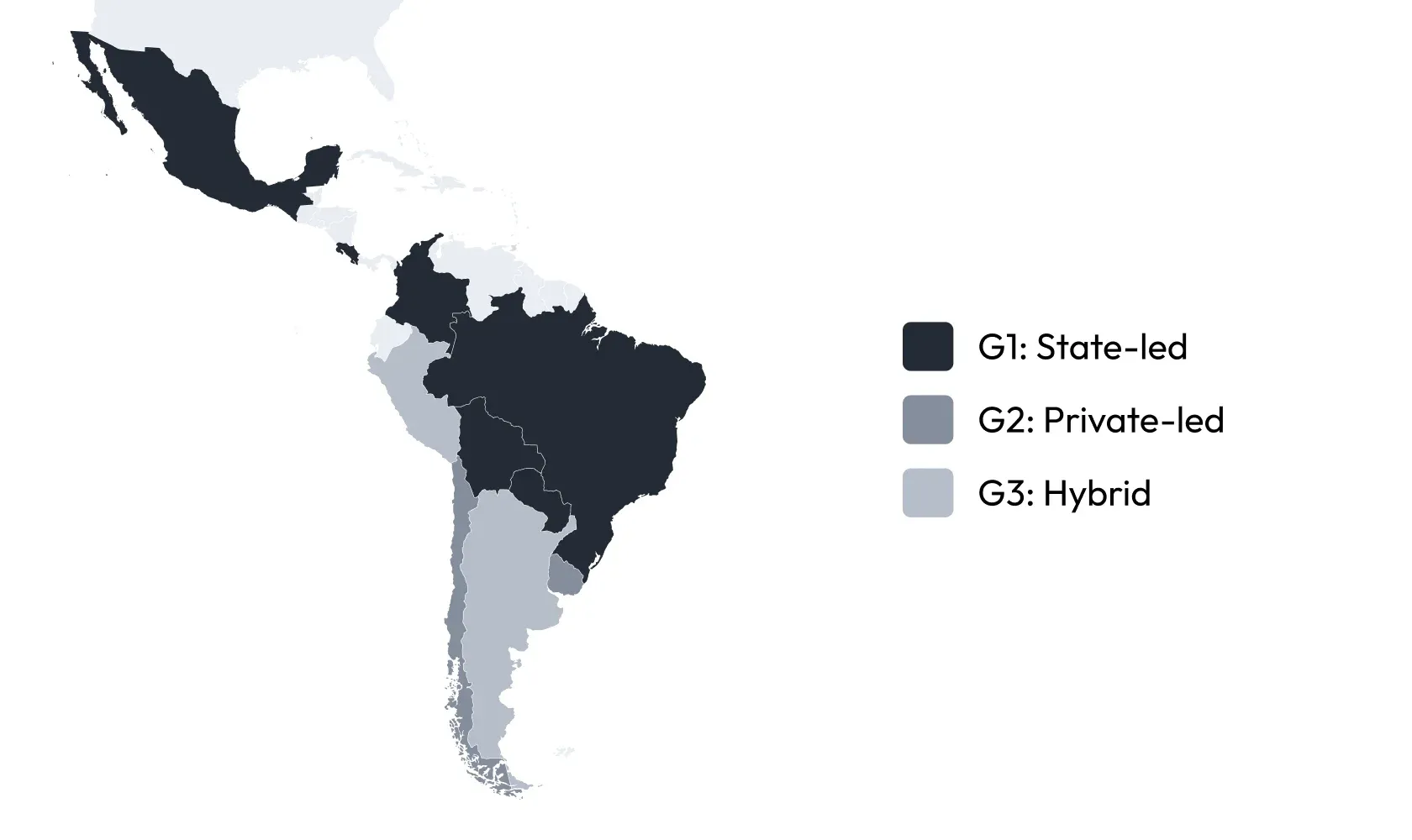

Broadly, three institutional models have emerged across the region.

Group 1: State-Led / Operated Models

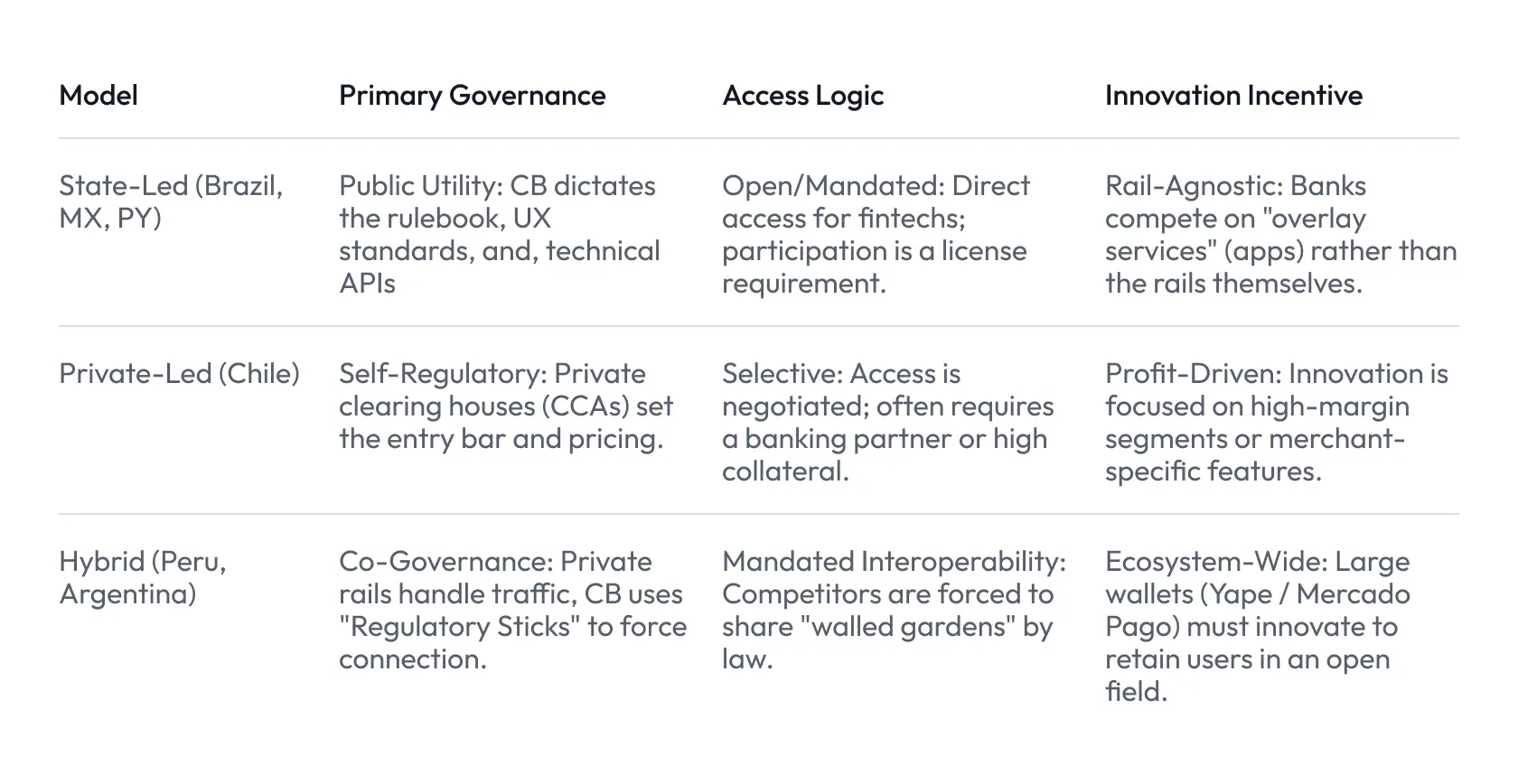

In state-led models, the central bank acts not only as regulator but also as system operator, positioning instant payments as a form of public infrastructure. Participation is often mandatory for large institutions, pricing is tightly controlled or eliminated for end users, and settlement typically occurs directly in central bank money.

The primary objective of this approach is rapid scale and universal reach, even at the expense of commercial flexibility. Brazil (Pix), Mexico (CoDi/DiMo), Colombia (Bre-B), and Paraguay (SPI) exemplify this model, with several Caribbean economies expected to follow a similar path.

Group 2: Private-Led / Market-Driven Models

Private-led models rely on competition and market incentives to drive adoption and innovation. In these systems, the central bank focuses on regulation, oversight, and settlement finality, while private clearing houses and banks operate the payment rails.

This approach tends to align more closely with commercial incentives and allows faster iteration, but often struggles to achieve universal interoperability without regulatory intervention. Chile and Uruguay illustrate this model, where payment innovation has been driven primarily by the banking sector rather than the central bank.

Group 3: Hybrid Models (Interoperability Mandates)

Hybrid models emerged where private innovation achieved rapid user adoption but also produced fragmented, closed ecosystems. In response, central banks intervened not by building new payment rails, but by imposing mandatory interoperability standards that forced existing systems to communicate.

Peru and Argentina represent this approach, combining private-sector execution with strong regulatory mandates to prevent market fragmentation and broaden access.

Centralization vs Modularity: Design Trade-offs in Latin American IPS

The differences in governance and architectural choices shape not only adoption outcomes, but also the distribution of operational, cybersecurity, liquidity, and standardization risks across the ecosystem.

Centralized IPS as Standard-Setters: Brazil and Mexico

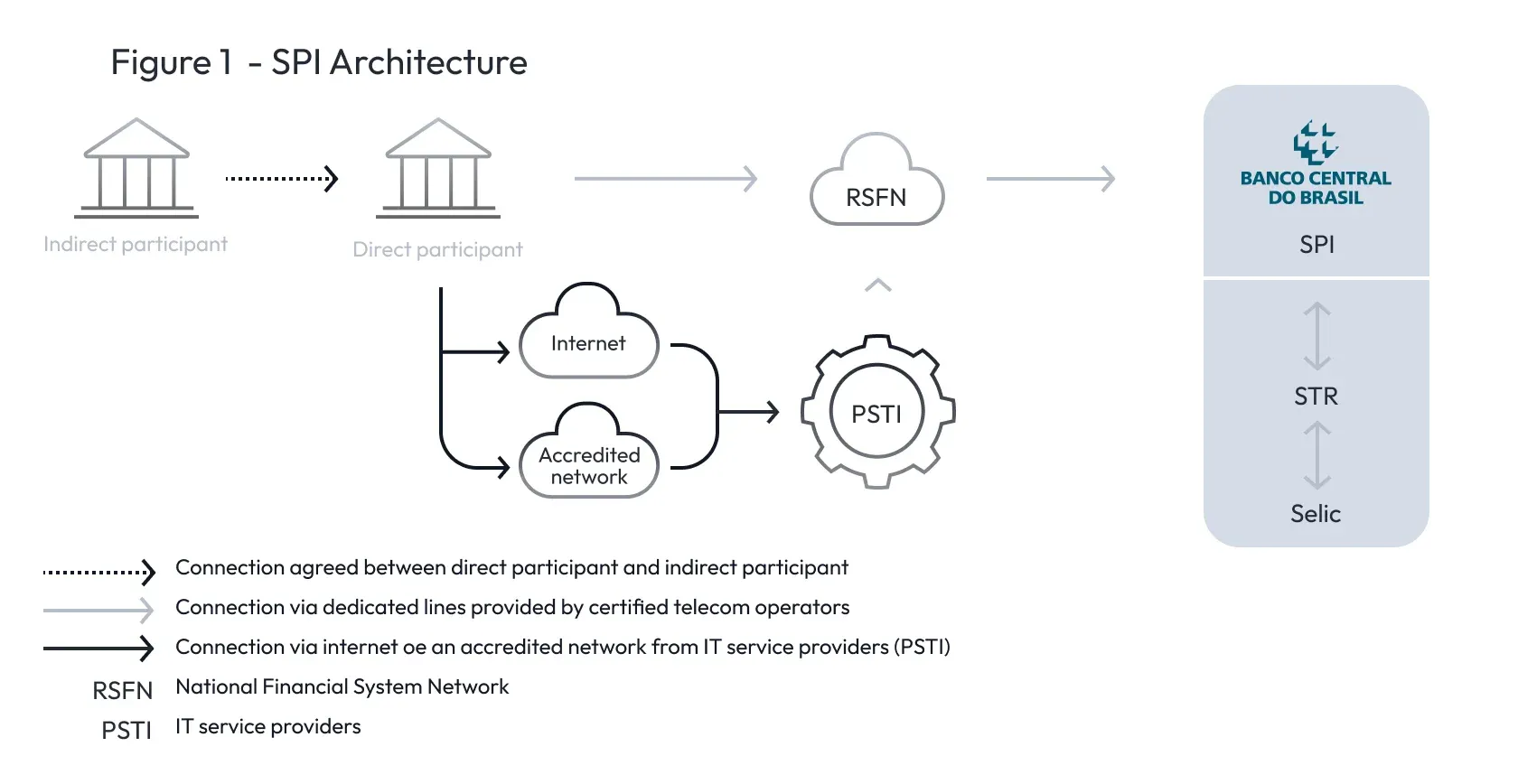

Brazil’s Pix stands as the region’s most prominent example of a centrally operated IPS. Managed by the Banco Central do Brasil, Pix has achieved near-universal adoption, reaching close to 90% of the adult population in just a few years. Its success lies in the central bank’s ability to act as both infrastructure operator and standard-setter, rapidly aligning banks, fintechs, and merchants around a single set of rules, identifiers, and user experiences.

However, this degree of centralization also concentrates risk. When retail payments are operated directly at the central bank level, operational and cybersecurity vulnerabilities at any infrastructure participant can propagate quickly into the core of the financial system. The 2024 C&M incident illustrated this risk clearly: a breach at a technology service provider enabled unauthorized access to settlement accounts held at the central bank, creating exposure with potentially systemic consequences. While such events do not negate Pix’s success, they highlight the trade-off between speed and scale on one hand, and risk concentration on the other.

Mexico presents a more nuanced picture. SPEI, the country’s real-time gross settlement system, has shown consistent growth and has become a reliable backbone for account-to-account transfers. Around SPEI, a vibrant fintech ecosystem has emerged, with players such as Clip and Konfío building strong capabilities in merchant acquisition, distribution, and acceptance. In contrast, CoDi — the state-led QR overlay launched in 2019 — has struggled to gain traction, with adoption hovering around 25% of the adult population.

This divergence suggests that while Mexico’s core rail has been successful, innovation and adoption at the retail layer have been driven primarily by market-led aggregators rather than by the public QR initiative. Concerns around usability, execution reliability, and the end-to-end payment experience appear to have undermined confidence in CoDi, even as private providers continued to scale on top of existing infrastructure.

Modular IPS with Private Clearing Layers: Chile and Peru

At the other end of the institutional spectrum lie countries that have deliberately avoided operating mass retail payments directly at the central bank. Chile is a clear example of this modular approach. The Chilean payment system separates wholesale settlement, handled by the central bank’s RTGS system, from retail clearing, which is performed by multiple privately operated low-value clearing houses. These include dedicated infrastructures for card payments as well as for electronic fund transfers serving P2P and P2B use cases.

This design significantly reduces liquidity, operational, and cybersecurity exposure at the central bank level. Risk is distributed across specialized, regulated private entities, while final settlement continues to take place in central bank money. The trade-off, however, emerges at the overlay layer. Because clearing is fragmented across multiple infrastructures, there is no single, immediately enforceable standard for services such as QR or NFC payments. Recent initiatives — such as BancoEstado’s “on-us” QR solution — demonstrate market dynamism, but extending these solutions to “off-us” scenarios requires coordination and standardization that naturally take time in a decentralized model.

Peru illustrates a related, but distinct, sequencing choice. Rather than launching a centralized IPS upfront, the Peruvian market saw the emergence of closed-loop digital wallets — notably Yape and Plin — well before the introduction of a formal interoperability framework (UPI). These wallets achieved significant scale independently, prompting the central bank to pursue a phased interoperability strategy, with Stage 1 launched in 2023. This bottom-up approach preserves competition and innovation, but it also implies a longer path toward full interoperability, as standards must be negotiated and implemented across already-established ecosystems.

IPS as a Public Utility and Liquidity Engine: Paraguay

Paraguay offers an instructive example of IPS treated explicitly as a public good. Since its launch, the country’s instant payment system has recorded growth of over 300%, achieving broad public acceptance and demonstrating the inclusion potential of a centrally coordinated approach. Yet this success also brings attention to a different layer of risk: liquidity management.

Because IPS operate continuously while RTGS systems typically do not, banks must either prefund their IPS positions, rely on extended intraday windows, or access central bank credit facilities to manage settlement flows during nights and weekends. As volumes grow, these mechanisms increase the central bank’s exposure to liquidity and credit risk. At a strategic level, this raises an important policy question: to what extent should central banks expand balance sheet exposure — including potentially granting broader access to settlement accounts — in order to sustain always-on retail payments?

Interim Assessment

Across these cases, no single institutional model emerges as unambiguously superior. Centralized IPS excel at rapid adoption and standard-setting but concentrate operational and balance-sheet risks. Modular architectures enhance resilience and preserve market-led innovation, yet slow the emergence of unified overlays. The critical test, therefore, lies not only in transaction volumes or adoption rates, but in how each design ultimately shapes fintech development and financial inclusion — the focus of the next section.

From Infrastructure to Impact: Fintech Development and Financial Inclusion

Institutional design shapes the path of fintech development and financial inclusion — but does not fully determine outcomes. Where public coordination is weak or fragmented, private aggregators often emerge as functional substitutes, though at the cost of delayed interoperability and uneven inclusion.

Adoption Is Not Usage: Wallet Penetration vs Habit Formation

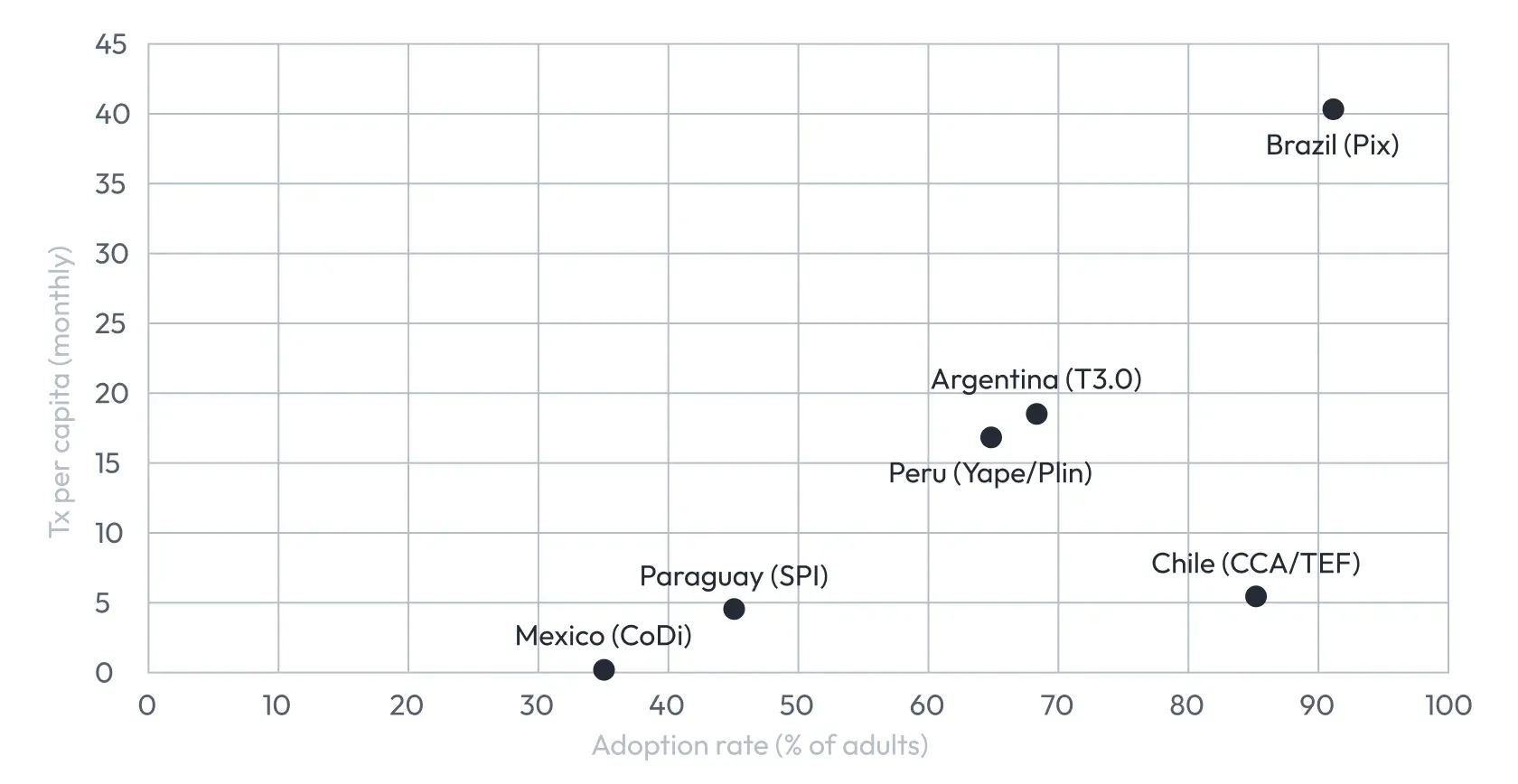

High registration rates do not necessarily translate into meaningful use. Countries with centralized, mandate-driven IPS have generally achieved faster onboarding, but usage intensity varies widely. Brazil stands out not only for adoption but for sustained transaction volumes per capita, indicating that Pix has become a habitual payment instrument rather than a contingency tool. Paraguay, despite lower income levels, shows a similar dynamic: rapid growth in usage suggests that treating instant payments as a public utility can materially change payment behavior.

By contrast, Mexico’s CoDi illustrates the limits of registration-led strategies. Although available nationwide since 2019, CoDi usage remains low relative to population size. This gap underscores a broader lesson: without trust, reliability, and merchant-side incentives, public overlays struggle to displace entrenched payment habits, even when underlying rails are robust.

When Public Coordination Falters, Markets Compensate

Low public overlay usage does not imply weak fintech ecosystems. Mexico is a leading fintech market in the region, with firms such as Clip and Konfío playing a central role in merchant acquisition, payments acceptance, and credit distribution. Rather than building atop CoDi, these players have developed proprietary acceptance networks and user experiences around existing rails. In effect, the market internalized coordination costs that public infrastructure did not resolve.

A similar dynamic appears in Chile and Peru, though through different paths. Chile’s fragmented clearing landscape has supported innovation and resilience, but slowed the emergence of unified retail standards. Peru’s dominant wallets, Yape and Plin, achieved scale in closed-loop form before interoperability mandates were introduced. In both cases, private actors solved immediate coordination problems, while regulators later moved to formalize interoperability.

These experiences suggest that fintech density and payment usage can grow even in fragmented environments, but often at the expense of universal access and seamless interoperability.

Cash Displacement as the Inclusion Benchmark

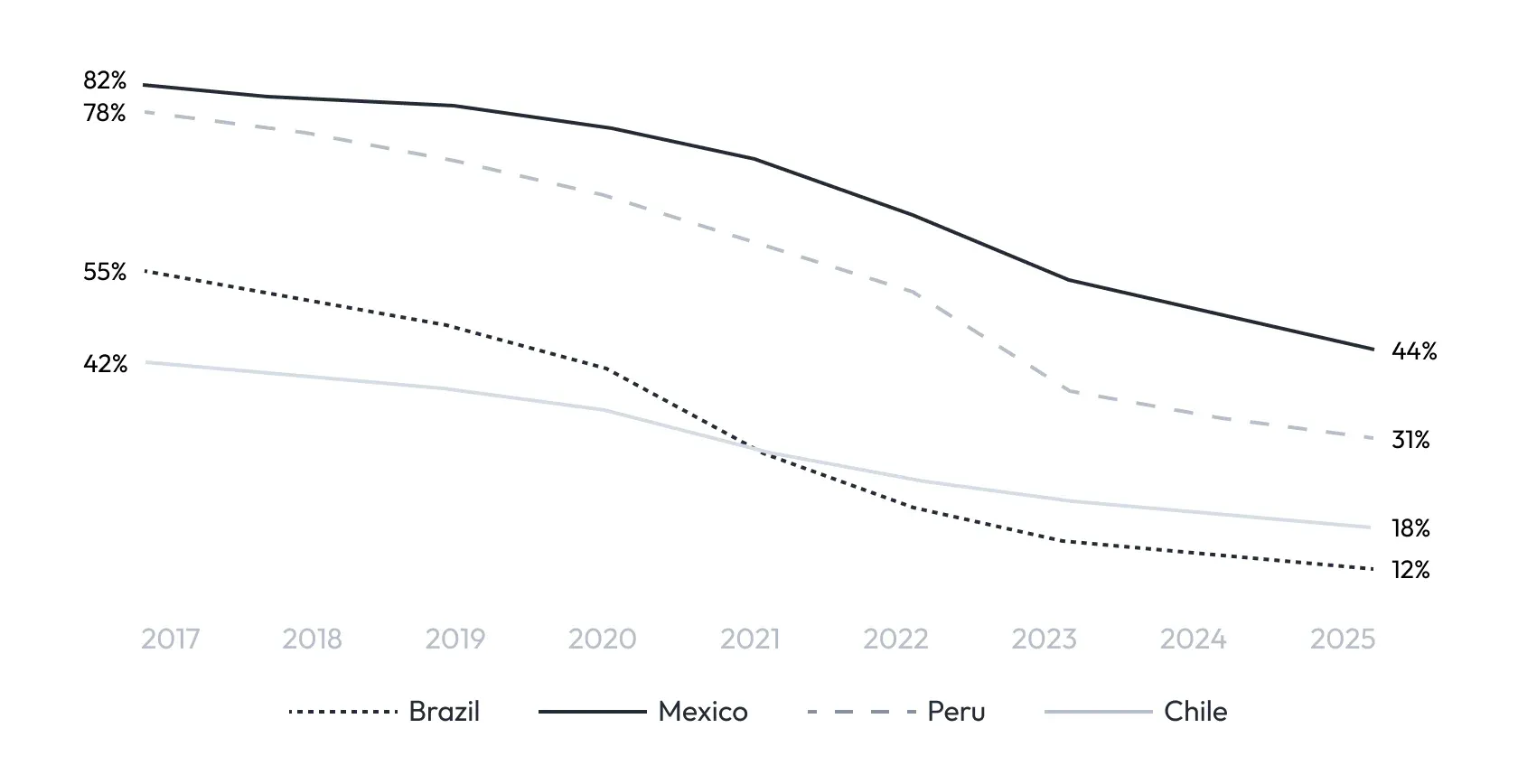

The most demanding test of financial inclusion is not wallet penetration, but sustained reductions in cash usage. Countries with high usage intensity in instant payments tend to show clearer declines in cash’s share of the monetary aggregate. Brazil and Paraguay exhibit the strongest patterns of cash displacement, consistent with their high-frequency use of account-based payments. Argentina, despite macroeconomic volatility, shows similar behavioral shifts where interoperable digital payments have gained traction.

Elsewhere, cash remains more resilient. In markets where payment ecosystems are fragmented or overlays lack trust, digital instruments coexist with cash rather than replacing it. This does not negate fintech progress, but it tempers claims of inclusion: true inclusion occurs when digital payments become the default, not the alternative.

The Take-Aways

Private Infrastructure is Viable (The Chilean Lesson)

The myth that only a Central Bank can run a national real-time rail has been debunked. Chile’s model proves that private clearing houses (CCA, Visa, Mastercard) can manage low-value payments with high resilience.

- The Recapitulation: By delegating the “plumbing” to the private sector, the Central Bank reduces its own cyber-concentration and liquidity risk. However, the trade-off is a slower path to universal standardization (QR/NFC).

Innovation can be Private-First (The Peruvian Lesson)

Peru’s Yape and Plin demonstrate that a country doesn’t need a state-built app to achieve financial inclusion.

- The Recapitulation: Innovation can be led entirely by private initiative, provided the regulator eventually steps in with a “Regulatory Stick” (the 2022 Interoperability Mandate) to break down walled gardens. This “Market-Led, State-Mandated” hybrid may actually be the most efficient path for developing economies.

Infrastructure is Not Adoption (The Mexican Paradox)

Mexico teaches us that having the most technologically advanced rail (SPEI) is meaningless if the retail overlay (CoDi) lacks public trust or merchant distribution.

- The Recapitulation: Credibility and execution failures can hinder growth even in a state-led system. In Mexico, the fintech ecosystem (Clip, Mercado Pago) succeeded by building around the state’s failures, proving that distribution is often more important than the infrastructure itself.

Final Thought: The Orchestration Frontier

The ultimate takeaway for 2026 is that there is no “perfect” institutional model. Brazil’s Pix offers unmatched scale but high central risk; Chile offers resilience but fragmented standards; Peru offers private agility but required a late-stage mandate to scale.

For businesses and fintechs, the challenge is no longer about which country has the “best” system, but about orchestrating across these diverse architectures. Success in Latin America now requires the technical flexibility to plug into a Central Bank rail in São Paulo, a private clearing house in Santiago, and a mandated wallet ecosystem in Lima.

Appendix